|

| Standardized Corporate Profits After Tax divided by GDP |

The main argument for profit margin mean-reversion is that high

margins invite new competition while low margins discourage new

entrants. Profit margins are also important to investors because steep reductions in profit margins tend to be coincident with steep

drops in corporate profits.

|

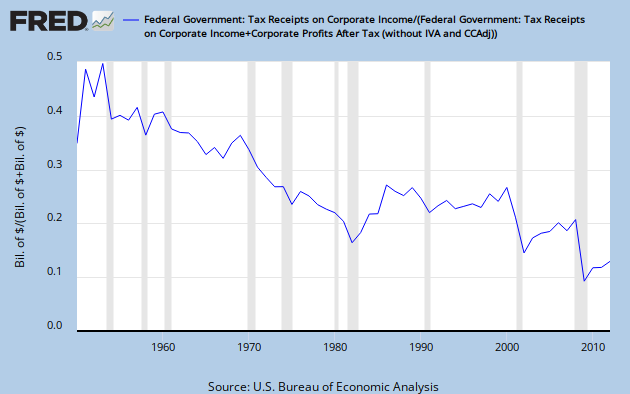

| Standardized Corporate Profits After Tax divided by GDP and Corporate Taxes as a % of Prior Peak |

{kind=link}

{kind=link}

Could it actually be the that maybe underlying margins on goods and services are not THAT high? Below you'll see a now similar chart which includes pre-tax corporate profits. As you can see, while pre-tax margins are elevated, they are much less alarming at +1.33 standard deviations and the rest is the effect of a near record low tax rate of 18.6%.

{kind=link}

(Note: above charts are quarterly and the one below is yearly since tax receipts are only available on a yearly basis.)

| ||

| Standardized Corporate Profits as % of GDP Before and After Tax |

With interest rates still falling and a multi-year liability repricing cycle, there is little immediate danger from a bottom in rates. Additionally, a fixed investment and/or employment boom which drove the cost of labor upwards would mean increases in final demand and GDP, leading to shrinking margins coupled with growing top-lines, not exactly a disaster.

Unless you see a recession in our very near future, it seems there's simply nothing to see here.

First of all, you shouldn’t be Cash Advance Guaranteed younger than 18, which is the obligatory demand for getting any type of credit, either you are going to get money via a bank or an alternative lender. Another requirement that is not less iPayday Loan Bad Credit mportant for being approved is a regular income that can be proved.

ReplyDeleteIn a world where power speaks volumes, beth dutton purse is her silent weapon—a stylish emblem of her unwavering dominance

ReplyDeleteFrom lighting installation to fuse board upgrades, we offer a wide range of electrical services in the UK ⚙️. Our team of professional electricians handles residential, commercial, and industrial projects with equal expertise. Whether you need fault finding, repairs, or complete system upgrades, we deliver safe, cost-effective, and energy-efficient electrical solutions for all types of properties ⚡.

ReplyDelete